Why expense ratio and exit load are very important in Mutual fund investment?

Mutual fund basics explained...

MUTUAL FUNDS

Expense ratio and exit load look like small numbers, but over long periods they quietly eat into returns and can reduce your final corpus by lakhs or even crores. Even a 1% higher cost can be the difference between hitting your wealth goal and falling short.

What is expense ratio?

The expense ratio is the annual fee a mutual fund charges for managing your money (management fees, admin, marketing, etc.).

It is expressed as a percentage of the fund’s total assets (for example, 0.5%, 1%, 2%).

It is deducted daily from the fund’s NAV, so you never see a separate “bill,” but your returns are lower than the gross return the portfolio earns.

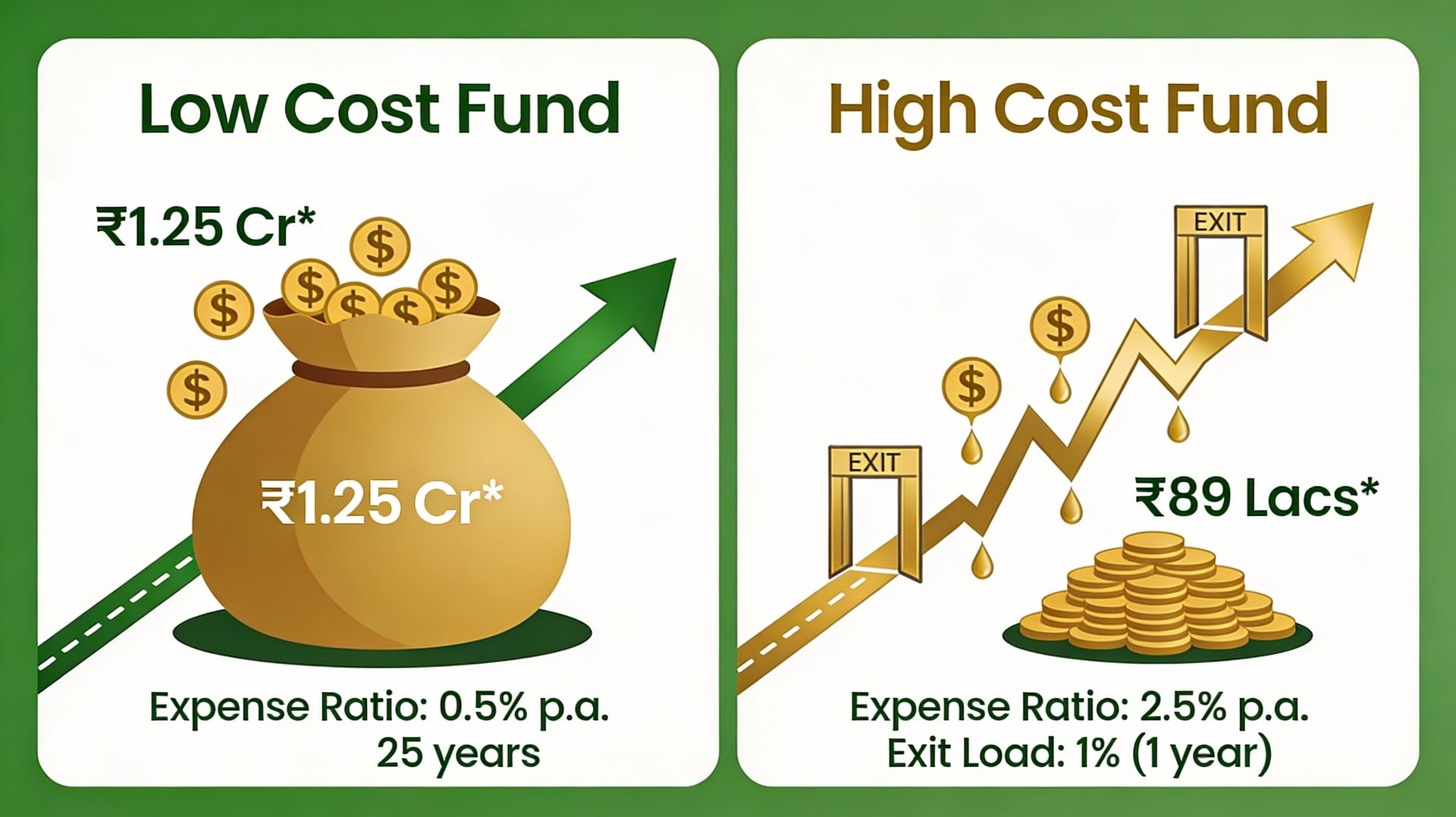

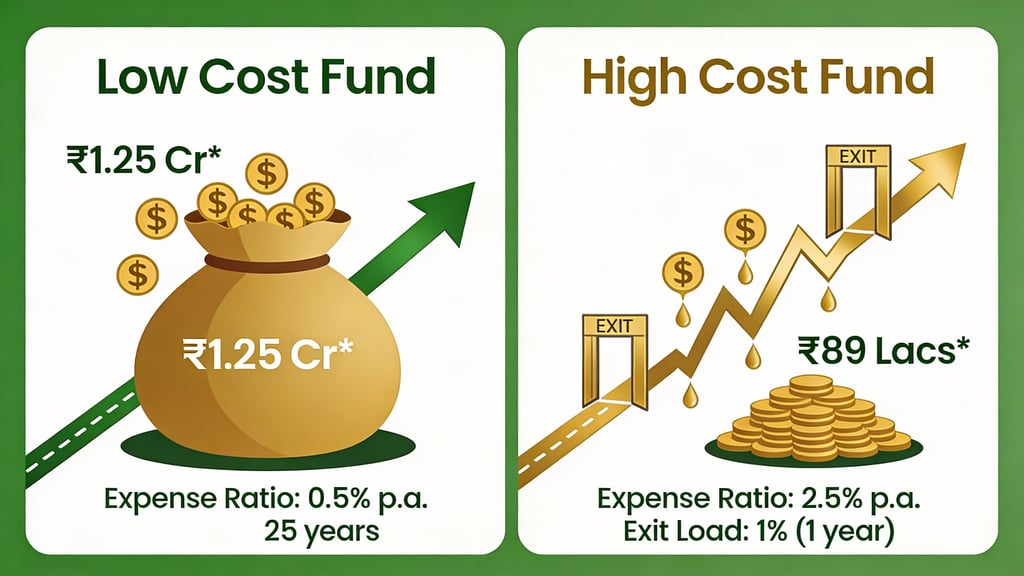

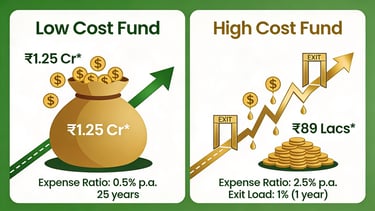

If two funds both earn 12% before costs, but one has a 0.5% expense ratio and the other 2%, your effective return becomes about 11.5% vs 10%. Over 20–25 years, that 1.5% gap compounds into a massive difference in your wealth.

What is exit load?

Exit load is a fee charged when you redeem (sell) your mutual fund units within a specified period.

Commonly, equity funds may charge around 1% if you exit before 12 months; after that, there may be no load.

It is deducted from the redemption value; for example, if your units are worth ₹1,00,000 and exit load is 1%, you receive ₹99,000.

Exit load is meant to discourage very frequent in-and-out behaviour and to protect long-term investors from the trading costs created by short-term investors.

How expense ratio affects long-term wealth

Compounding works on what you keep after costs, not on the headline market return.

Consider two investors putting ₹10,000 per month for 25 years:

Investor A in a fund earning 12% with 0.5% expense (net ~11.5%).

Investor B in a similar fund earning 12% with 2% expense (net ~10%).

The difference of just 1.5% per year can lead to a gap of tens of lakhs or more in the final corpus. The higher-cost fund is not only more expensive each year, it also reduces the base on which your future returns compound. Choosing consistently lower expense ratios—especially in index funds and large-cap funds—lets more of the market’s return stay in your pocket.

How exit load affects your behaviour and returns

Exit loads mainly hurt when you keep jumping in and out of funds.

If you redeem frequently within the exit-load period, each exit quietly shaves off a part of your capital.

This cost is on top of any tax you may pay on short-term capital gains.

Knowing there is an exit load can also nudge you towards more disciplined, long-term holding instead of panic selling after short-term volatility.

For long-term SIP investors who stay beyond the exit-load period, exit load usually has very little impact—but if your behaviour is very reactive, it can become a recurring drag.

Why serious wealth builders must care

If your goal is long-term wealth building (retirement, financial freedom, kids’ education):

A difference of 1–2% per year in costs (expense ratio + frequent exit loads) over 20–30 years can reduce your final wealth by a very large amount.

Lower-cost, well-diversified funds give you more of the market return and rely on discipline rather than constant “high-return” promises.

Before investing, always check both the expense ratio and the exit load structure in the scheme information document and compare with similar funds.

In short: returns are uncertain, but costs are guaranteed. You cannot control the market, but you can control how much you pay to participate in it, and that decision has a powerful effect on your long-term wealth.

Help

Questions? Reach out anytime.

reachus@69waystoinvest.com

© 2026. All rights reserved.

Our Team-

Shrinivas B(MBA)

Ravi (MBA)

Prasad (Mcom)